For years, the phrase “Data is the new oil” was thrown around as a vague corporate cliché. Today, that narrative has shifted from an abstract marketing pitch into a measurable, techno-legal reality. Driven by incoming international accounting frameworks, local regulatory mandates, and indigenous governance models, India is establishing a structured environment where data is recognized not just as an operational by product, but as a quantifiable financial asset.

Evaluating the multi-layered initiatives across India reveals how different agencies are approaching data valuation, along with their current operational status.

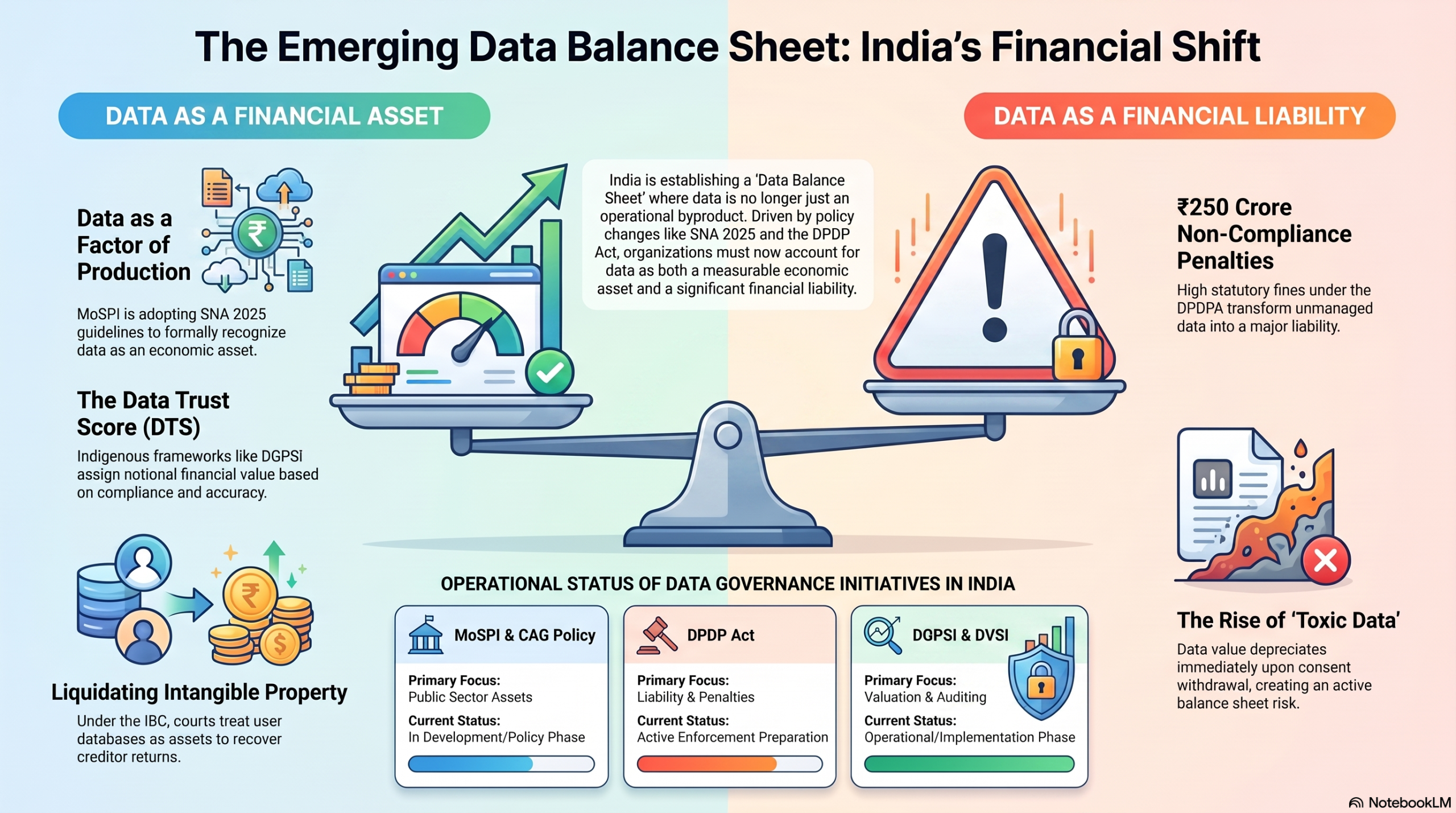

1. Macro-Government & Policy Initiatives: The Public Sector Shift

The government has recognized that to build a true digital economy, the state must find a uniform way to measure digital assets.

-

MoSPI and SNA 2025 Adoption: The Ministry of Statistics and Programme Implementation (MoSPI) has actively engaged with the United Nations System of National Accounts (SNA 2025) guidelines. These standards formally recognize data as an economic factor of production. Government committees are currently outlining how public sector undertakings (PSUs) should officially categorize and track data assets.

-

The CAG Mandate: The Comptroller and Auditor General (CAG) of India has signalled a clear need to capture the intrinsic value of data repositories within public asset reporting.

-

Current Status: In Development/Policy Phase. Draft frameworks are under review to determine how state-owned data exchanges and infrastructure datasets can be accounted for without compromising national security or individual privacy.

2. Regulatory Compliance Drivers: The DPDP Act & Toxic Data

The rollout of the Digital Personal Data Protection Act (DPDPA) has upended traditional data accumulation strategies. Data valuation in India can no longer be evaluated through the lens of potential monetization alone; it must be balanced against statutory liability.

-

Asset vs. Liability Dynamics: With penalties reaching up to ₹250 crore per non-compliance instance, unconsented, poorly structured, or “zombie” data is no longer an asset—it is an active balance sheet liability.

-

Current Status: Active Enforcement Preparation. Organizations are actively filtering their datasets to compute their “clean data” volume. Under this model, data value dynamically depreciates the moment a Data Principal withdraws consent or the processing purpose expires.

3. Indigenous Institutional Frameworks: DGPSI and DVSI

While traditional accounting standards (like Ind AS 38) remain highly conservative about capitalizing internally generated data, pioneering frameworks within India have stepped forward to fill the gap.

-

Data Governance and Protection Standard of India (DGPSI): Developed by FDPPI, DGPSI has embedded financial data valuation directly into its governance specifications. Specifically, Model Implementation Specification 9 (MIS-9) explicitly requires organizations to establish a policy assigning a notional financial value to distinct datasets. This ensures the board has visibility into the economic worth of the data assets they oversee. DGPSI’s metric—the Data Trust Score (DTS)—serves as a core indicator of how compliance directly protects and enhances an asset’s baseline value.

-

Data Valuation Standard of India (DVSI): Operating alongside DGPSI, the DVSI model introduces a specialized two-stage valuation methodology. It calculates the intrinsic cost of data (using classic cost of acquisition or market parameters) and applies a dynamic multiplier index based on legal compliance, data accuracy, and cryptographic protection.

-

Current Status: Operational/Implementation Phase. The newly launched Association of Independent Data Auditors (AIDAI) is actively training and empanelling Certified Independent Data Auditors (CIDAs) to handle data audits that combine compliance testing with these advanced data valuation techniques.

4. Valuation in Insolvency and Distress: The IBC Track

The most concrete financial realizations of data value are currently occurring under distressed corporate conditions.

-

Insolvency and Bankruptcy Code (IBC), 2016: Resolution Professionals (RPs) and Registered Valuers regularly encounter scenarios where a failed startup, fintech platform, or e-commerce provider holds minimal physical assets, but possesses massive, highly structured user databases and proprietary transaction algorithms.

-

Current Status: Fully Functional Legal Practice. Courts and liquidators treat these data stacks as intangible corporate property under Section 36 of the IBC, utilizing Income or Market-driven slump sales to maximize recovery returns for creditors.

Reconciling Value and Responsibility: The “Data Balance Sheet”

The convergence of these initiatives points toward a inevitable destination: the Data Balance Sheet. Under a double-entry governance framework, personal data under management must be accounted for simultaneously as an economic asset and a corresponding contingent liability (accounting for potential data breaches, regulatory fines, and remediation costs).

Organizations that wait for standard accounting boards to hand down a rigid template will find themselves exposed to severe regulatory and financial risks. Relying on frameworks like DGPSI to understand exactly what data you possess, what value it generates, and what risks it carries is no longer just a compliance choice—it is a baseline requirement for modern corporate sustainability.

(To Be continued)

Naavi

")