(This is in continuation of the previous article on Evolution of Data Valuation in India)

DGPSI Full version has indicated a model implementation specification which states

“Organization shall establish an appropriate policy to recognize the financial value of data and assign a notional financial value to each data set and bring appropriate visibility to the value of personal data assets managed by the organization to the relevant stakeholders.”

So far this has remained a suggestion which is more to indicate the auditee that they need to move in this direction. But with CAG guidelines for PSU auditors, the time has come to expand this MIS into a draft policy.

A tentative attempt is made in this direction to present a draft policy here for further discussion.

This draft policy takes into account Naavi’s Theory of Data and Data Valuation Standard of India as supporting documents.

This is work in progress and Comments are welcome.

We can discuss this during our Chennai Seminar on July 17th 2026.

Quote:

Applicability: All business units, data repositories, and processing operations handling Personal Data.

Framework Alignment: DGPSI Model Implementation Specification 9 (MIS-9) & Data Valuation Standard of India (DVSI)

1. Purpose & Objective

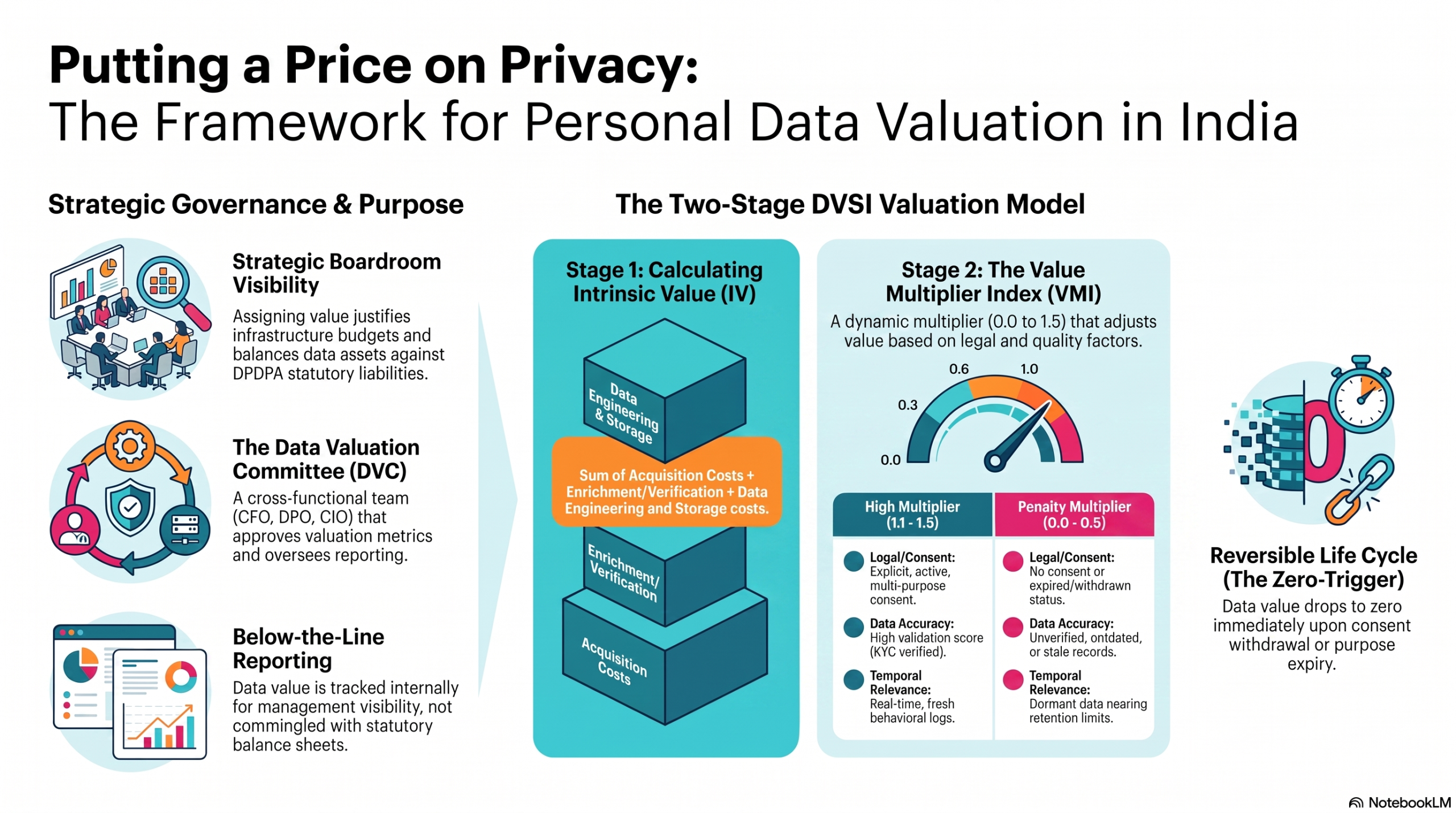

In accordance with Model Implementation Specification 9 (MIS-9) of the Data Governance and Protection Standard of India (DGPSI) framework, this policy outlines a structured, techno-legal mechanism to recognize, compute, and track the financial value of personal data assets under management.

By assigning a notional financial value to internal personal datasets, this organization aims to:

-

-

Bring strategic boardroom visibility to the economic importance of Data Governance and Protection.

-

Justify and allocate proportionate resources, budgetary tools, and infrastructure to safeguard data.

-

Balance corporate data assets directly against corresponding operational and statutory liabilities under the Digital Personal Data Protection Act (DPDPA).

-

2. Scope

This policy applies to all structured and unstructured personal data sets acquired, generated, processed, or stored by the organization in its capacity as a Data Fiduciary or Data Processor. It covers both active consumer/client databases and historical, administrative, or employee records.

3. Governance Structure

To maintain accountability, a formal data valuation hierarchy is established:

-

-

Data Valuation Committee (DVC): A cross-functional oversight committee comprising the Data Protection Officer (DPO), Chief Financial Officer (CFO), Head of Internal Audit, and Chief Information Officer (CIO). The DVC is responsible for approving specific valuation metrics annually.

-

Data Valuation Officer (DVO): A designated operational role tasked with executing asset measurements, maintaining the Centralized Personal Data Inventory, and reporting periodic asset fluctuations to the DVC.

-

4. Valuation Methodology: The Two-Stage DVSI Model

To ensure calculations are robust and defensible during third-party data audits, the organization adopts the Data Valuation Standard of India (DVSI) two-stage valuation protocol.

[ STAGE 1: INTRINSIC VALUE (IV) ]

Computed via Cost of Acquisition or Market Replacement

│

▼

[ STAGE 2: VALUE MULTIPLIER INDEX (VMI) ]

Adjusts value based on Consent, Accuracy, Age, and Sensitivity

│

▼

[ FINAL NOTIONAL DATASET VALUE ]

Stage 1: Determination of Intrinsic Value (IV)

The baseline value of a dataset is calculated using the Cost-Based Method, capturing the direct financial outlays incurred to build the asset:

Where market metrics are readily available (e.g., commercial marketing registries or structured platform logs), a Market-Replacement approach may be utilized subject to DVC approval.

Stage 2: Application of the Value Multiplier Index (VMI)

To bridge the gap between financial cost and regulatory compliance, the Intrinsic Value must be adjusted dynamically by a multiplier matrix () that scores the legal and operational quality of the personal data:

The VMI is computed by evaluating four distinct criteria:

Legal / Consent Status

Explicit, verifiable, and active consent recorded for multi-purpose utilization.Valid consent for a singular, ongoing operational purpose.No Consent / Restricted Use: Data processed under high-risk grounds or where consent is withdrawn/expired ().

5. DPDPA Reversible Life Cycle & Financial Depreciation

Unlike conventional corporate assets, the value of personal data is fully reversible. The life cycle dictates strict rule-based depreciation tracking:

-

-

Consent Withdrawal Depreciation: If a Data Principal exercises their right to withdraw consent under the DPDPA, the financial value of that specific record immediately drops to zero () and must be deleted.

-

Purpose Expiry Depreciation: The moment the specified purpose for processing is fulfilled, the dataset’s multiplier falls to zero, forcing its removal from the active asset register.

-

The Compliance Premium: Datasets that achieve a high Data Trust Score (DTS) via independent third-party validation receive a positive valuation weighting, reflecting their minimized liability exposure.

-

6. Reporting and Visibility

-

-

Below-the-Line Financial Visibility: The final aggregated notional value of personal data assets shall be maintained on an internal management register and presented as a “below-the-line” item alongside corporate financial reporting. It shall not be commingled with standard statutory balance sheet line items unless acquired through an M&A transaction.

-

Board Level Disclosure: The DPO and CFO shall jointly submit a biannual Data Asset and Risk Report to the Board of Directors, detailing the shifting monetary value of the enterprise’s data holdings alongside estimated statutory liability exposures.

-

7. Audit and Review

This policy and its active calculations are subject to independent review during annual data audits conducted by Certified Independent Data Auditors (CIDAs) using the DGPSI-Full verification framework.

Unquote

Naavi

Also refer: Research paper on Data Valuation- Mr Peter Walsh

")