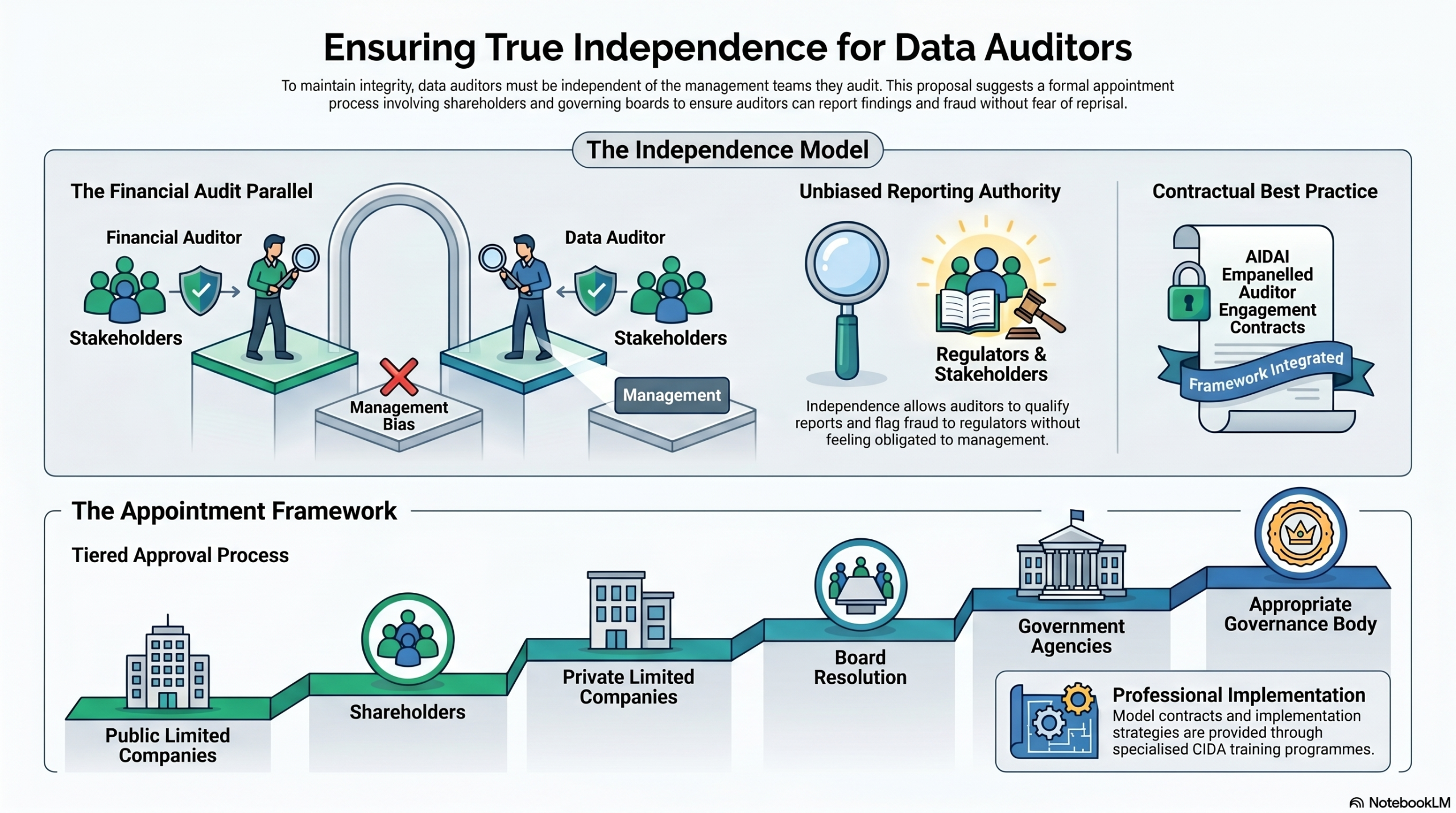

We are aware that one of the aspects that supports independence of a financial auditor is because the statutory financial auditor is appointed by the share holders of a company. Hence the Auditors are able to qualify the report if required and also report frauds to the regulatory authorities without feeling obligated to the management which may fix their remuneration.

Naavi would like to propose a similar scheme for Independent Data Auditors. What this practically means is that the Independent Data Auditor appointed by a Significant Data Fiduciary should be approved by the share holders of a company (in the case of public limited companies) or through a Board resolution (In the case of private limited companies) and an appropriate Governance body in the case of Government agencies.

Initially this will be suggested in the engagement contract which an AIDAI empanelled auditor would like to obtain from the management of a company.

This will be a best practice suggestion for the drafting of the engagement contract (a suggested model contract of which will be shared in the CIDA training.)

Naavi

")