We are all aware of the Financial Accounting system where we prepare an annual revenue and expenditure statement, Funds Flow or Cash Flow statements and Balance Sheets.

Naavi opens up a debate on whether it is possible to develop a Balance sheet for “Data Assets” of an organization on similar principles.

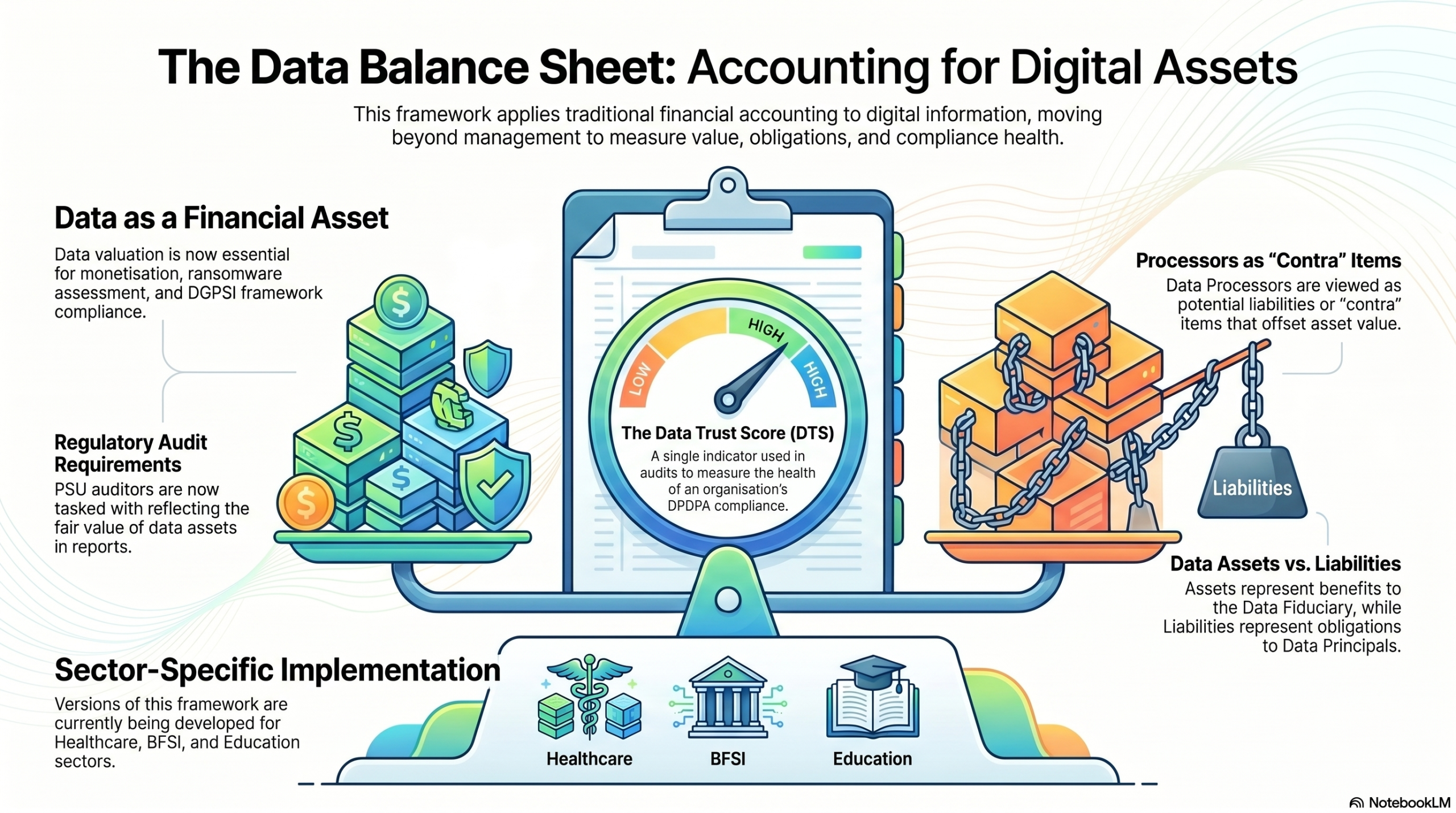

“Data is an Asset” is now an accepted principle. The fact that it has a financial value is know even to hackers who place a ransomware price on it. Data Monetization depends on such value.

DGPSI framework requires Data Valuation to be assessed. CAG has also asked PSU auditors to reflect a fair value of Data Assets in their audit reports.

The system of DTS (Data Trust Score) is part of DGPSI based audits and is a single indicator of the health of DPDPA compliance of an organization.

Beyond this Naavi now introduces a new thought. Can we draw a list of Data Assets of an organization as on a particular day and assign a notional value?

Can we develop a concept of “Asset” and “Liabilities” for Data… in the form of obligations to the Data Principals vs benefits to the Data Fiduciary? Are Data Processors a “Liability”? like a “Contra” item?

Possibilities are interesting.

This could be an extension of the “Theory of Data” which Naavi has already proposed.

Presently Naavi is busy working on DGPSI-Versions for Healthcare, BFSI and Education Sector. The concept of “Data Balance Sheet” will also be developed as we go ahead.

Watch out for more on this concept in these columns.

P.S: This is an idea under development. Be prepared for refined versions to be posted in due course.

Naavi

Video Overview:

")