I have recently raised an issue about non receipt of NOC for an Auto loan closed in 2018. The brief description of the incident is as follows:

I am placing these in public domain as it indicates that even a Bank like HDFC Bank is currently not ready for DPDPA Compliance by 13th may 2027.

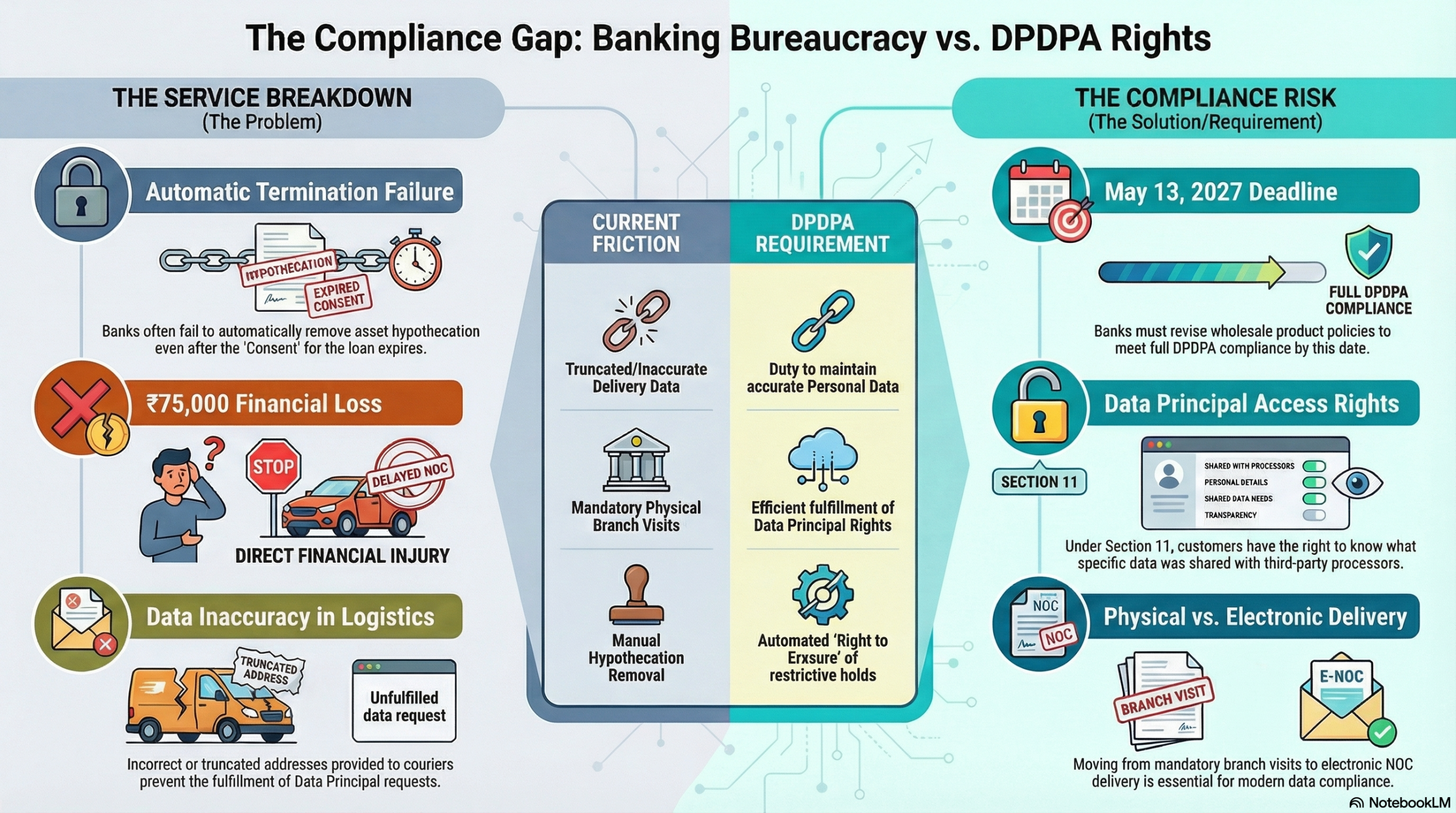

Everybody is running behind Consent forgetting that handling Data Principal access requests is a key element of compliance and cannot be fulfilled without a wholesale revision of the product policies.

Quote:

Dear Sir

For the last few days, I have been corresponding with your loan products department and customer services department and am unable to get resolution of my problem. I am therefore bringing this to your notice for redressal as a “Grievance” and “Data Principal Right”.

The incident is briefly described below.

1. I had availed an auto loan in 2013 which closed in 2018.

2.On closure of the loan I was under the assumption that the Bank has ceased to be the hypothecatee of the vehicle since the “Consent” was terminated automatically. It was therefore a duty of the Bank to have taken measures to inform the RTO and delete the hypothecation clause. The RC certificate/card with me was not indicative of any hypothecation and hence I was not aware that the Bank was still actively placing a restrictive hold on the asset which should have been free.

3. Recently I tried to put my car on sale and invited bids from intended buyers. I got some offers which were good enough for me to accept. However I was told by the buyer that since there was a hypothecation on the vehicle, it needs to be removed. I then submitted a request for NOC. Given that I am a customer for decades and on my customer account the loan also is on record, I thought that the issue of NOC should be quick.

4. I got a message from Bluedart courier that a consignment was being delivered and assumed that it should be the NOC. But I found after a few days that there was no delivery of the letter and my commitment to submit the letter to the buyer by a certain date was frustrated.

5. On calling the Blue Dart courier, I was told that they could not deliver and they had noted that “Addressee was not available at the given address”. When I enquired how they marked such a note which was a “Lie”,

6. Even after raising the issue with the Bank, I am yet to see resolution.

In this context my questions to you as the DPO of the bank is as follows.

1.You have the account details under my customer ID which also has the loan details. My address is updated on this account page. Hence the claim of Bluedart that a truncated address was only available with them (They claim that the name was simply mentioned as “Nagaraj”) should be false. I would like to know from your records what is the address given to Bluedart for the delivery of the consignment and why it was not given correctly is their statement is true?. This may be considered as a request under Section 11 of DPDPA 2023. (As part of Section 43A read with DPDPA as the Due diligence requirement).

2. Why do the courier say they did not have my phone number to contact? Was it not given by HDFC Bank? If Not why?

3. Non availability of the NOC has frustrated the sale of the vehicle to a preferred buyer and has perhaps inflicted a financial loss of Rs 75000/- since I have to now sell it to another buyer and after March 31st. Please let me know why I cannot claim this as a compensation either as deficiency of service or under Section 46 of ITA 2000.

4. I was disappointed that HDFC Bank has failed to maintain the simple courtesy of removing the hypothecation after a loan closure which should have been a customer service move. Why this is not a SOP? Why do you expect the customer to complete it himself under these circumstances of service deficiency? I am told by many that this is a common problem of many.

5. I was told by your help center that NOCs can only be obtained by physically visiting one of the three designated branches in Bangalore (Not the nearest Branch). Why is HDFC bank not able to deliver the NOC electronically?

6. Has your Bank initiated any steps for DPDPA Compliance so far? …It appears that you will not be ready by May 13 2027 and will be exposed to penalties under DPDPA. Has this risk been flagged by your CFO under disclosures under Clause 49 of listing requirements and SEBI regulations?

For the education of the public, I will be placing these questions in the public domain through www.naavi.org

Looking forward to your response.

End Quote

I will be happy to receive your comments.

Naavi

")