The above Economic Times report on MoSPI’s proposal to treat Data as an Asset provides independent validation of a principle that FDPPI incorporated into DGPSI as early as September 2023, namely that personal data possesses measurable economic value and therefore requires both governance and valuation. The Data Valuation Standard of India (DVSI), developed alongside DGPSI, specifically focused on methodologies for valuing personal information assets and assessing the corresponding liability exposure arising from their misuse, loss or unauthorized processing. (P.S. Under DVSI, we have focussed only on the valuation of Personal Information).

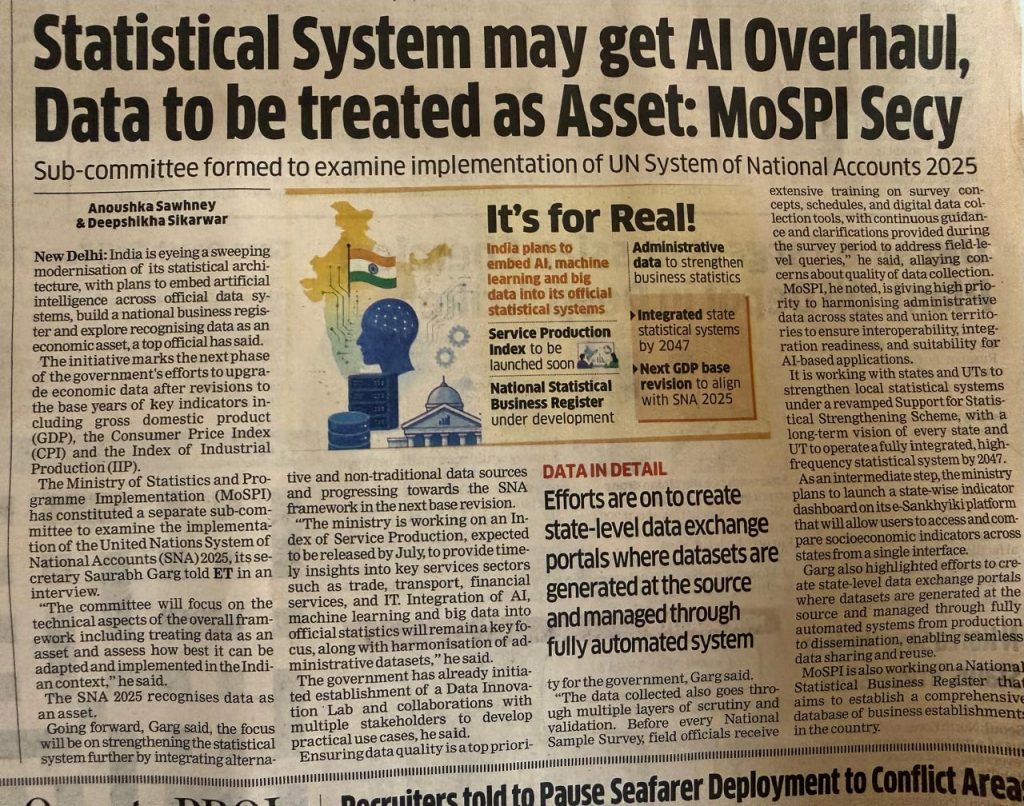

The statement of the Secretary, Ministry of Statistics and Programme Implementation (MoSPI), reported in the above article of Economic Times, that India is examining the implementation of the United Nations System of National Accounts (SNA) 2025 and exploring the treatment of “Data as an Asset” deserves the attention of every privacy professional, Data Protection Officer and Data Auditor in the country. This follows the CAG indicating the need to represent value of Data in the PSU asset reporting. (Refer here)

According to the report, a dedicated sub-committee has been constituted to study the implications of SNA 2025, which formally recognizes data as an economic asset.

Simultaneously, the Government plans to integrate Artificial Intelligence, Machine Learning and Big Data into official statistical systems, establish a National Statistical Business Register, and create interoperable data exchange systems across States and Union Territories.

While this may appear to be a new policy direction, professionals associated with DGPSI (Data Governance and Protection Standard of India) would recognize that the concept of “Data Valuation” has already been embedded within the DGPSI framework as a recommended best practice for DPDPA compliance.

Data Protection and Data Value: Two Sides of the Same Coin

Most organizations approached DPDPA compliance initially from a defensive perspective.

The focus was on:

- Avoiding penalties.

- Managing consent.

- Handling data principal rights.

- Implementing security safeguards.

- Establishing governance structures.

However, DGPSI has consistently advocated that organizations should not view personal data merely as a compliance burden. Personal data is simultaneously:

- A regulated asset carrying legal obligations.

- A business asset carrying economic value.

An organization that understands only the compliance dimension of personal data will always see privacy as a cost centre. An organization that understands both compliance and value dimensions can transform privacy governance into a business enabler.

It is for this reason that DGPSI introduced the concept of Data Valuation as part of its governance philosophy.

Why Data Valuation Matters

Traditionally, organizations record physical assets, financial assets and intellectual property assets in their books of account. Yet, in the digital economy, data often contributes more to enterprise value than many tangible assets.

A customer database, behavioural analytics repository, transaction history archive, AI training dataset or reputation profile may represent substantial economic value.

At the same time, these assets also create legal liabilities.

Therefore, a mature governance framework requires organizations to understand:

- What data they possess.

- Why they possess it.

- What value it creates.

- What risks it creates.

- Whether the value generated justifies the compliance costs and associated liabilities.

DGPSI therefore encourages organizations to move beyond data inventory and progress towards data valuation and data risk quantification.

SNA 2025 and the Emergence of a Data Economy

The significance of the MoSPI announcement lies in the fact that the Government is now considering the same issue at the national level.

If data becomes recognized as an economic asset within national accounting systems, several important developments may follow:

- Recognition of data creation as an economic activity.

- Development of methodologies for measuring data value.

- Inclusion of data-related assets in economic productivity calculations.

- New policy frameworks for data sharing and reuse.

- Greater emphasis on data quality, authenticity and governance.

This represents a shift from viewing data merely as information to viewing data as an economic resource.

The transition is comparable to the historical evolution whereby intellectual property moved from being an abstract legal right to a recognized economic asset.

Towards a Data Balance Sheet: Reconciling Data Value and Data Responsibility

Naavi has previously proposed the concept of a “Data Balance Sheet”, under which personal data is represented simultaneously as an economic asset and a corresponding liability within a double-entry governance framework. While still under development, the concept offers a possible bridge between data economics and data protection jurisprudence.

Traditional accounting systems record assets and liabilities arising from tangible property, financial instruments and contractual rights. However, in the digital economy, personal data simultaneously creates value and obligations.

Naavi’s emerging concept of a “Data Balance Sheet” seeks to recognize this duality.

Under this approach:

Personal data under management is recognized as a data asset.

Potential compensation claims, regulatory penalties, reputational damage and remediation costs may also be reflected as contingent data liabilities.

Data quality improvements increase asset value.

Privacy risks, security vulnerabilities and compliance deficiencies increase liability valuation.

Such a model would align naturally with the fiduciary philosophy of DPDPA and could eventually become an important governance tool for boards, auditors and regulators.

The DPDPA Perspective

The recognition of data as an asset must however be approached carefully.

DPDPA 2023 deliberately adopts a fiduciary model rather than a property model.

Under DPDPA:

- The Data Principal enjoys legal rights over personal data.

- The Data Fiduciary receives limited authority to process data for specified purposes.

- The relationship is governed by trust and accountability rather than ownership.

Consequently, recognizing data as an economic asset cannot be interpreted as granting ownership rights for the data fiduciary over personal data to organizations or Governments.

The economic value of data must coexist with the legal rights of Data Principals.

This is likely to become one of the most important jurisprudential debates of the coming decade.

Implications for Data Auditors

The recognition of data as an asset has direct implications for the emerging profession of Independent Data Auditors.

Future audits may need to examine not only:

- Compliance with DPDPA.

- Security safeguards.

- Consent management.

- Data lifecycle management.

but also:

- Data quality.

- Data lineage.

- Data valuation methodologies.

- Data governance maturity.

- AI training data governance.

- Economic impact of data assets.

The Independent Data Auditor of tomorrow will therefore require multidisciplinary competence covering law, technology, governance, statistics and economics.

DGPSI’s Early Recognition

The significance of the present development is that it validates the broader vision underlying DGPSI.

Long before the national statistical system began discussing “Data as an Asset”, DGPSI had already recognized that organizations need mechanisms to assess both the value and risk associated with the data under their control.

The Government’s present initiative indicates that India is moving towards a future where data will be simultaneously viewed as:

- A subject of rights.

- A source of accountability.

- A factor of production.

- An economic asset.

Organizations that have already adopted DGPSI principles will find themselves better prepared for this emerging paradigm.

DGPSI’s approach differs fundamentally from conventional accounting approaches. It treats data valuation not merely as an exercise in asset recognition, but as an exercise in fiduciary governance. The objective is not simply to measure value, but to measure responsibility associated with that value. That distinction would differentiate DGPSI from conventional accounting approaches and strengthen the argument that DGPSI anticipated the policy direction now emerging through SNA 2025.

SNA 2025 recognizes data as an economic asset for national accounting purposes.

DPDPA recognizes personal data as an object of fiduciary responsibility.

The challenge before policymakers is to ensure that the economic valuation of data does not dilute the rights of Data Principals.

However when Naavi’s concept of Data balance sheet gets developed, the situation may undergo another paradigm shift.

In summary,

The MoSPI initiative should not be viewed merely as a statistical reform. It represents a conceptual shift in the Indian digital economy.

The question is no longer whether data has value.

The question is how that value should be measured, governed, protected and shared while preserving the rights of Data Principals.

As India moves towards implementing SNA 2025 and integrating AI into official statistical systems, the relevance of robust governance frameworks such as DGPSI will only increase.

The future belongs to organizations that can demonstrate not merely possession of data, but accountable stewardship of valuable data assets.

Just as environmental accounting evolved from a peripheral concept into ESG reporting, data valuation may evolve from a governance practice into a mandatory reporting requirement.

The day may not be far when annual reports carry a certified Data Balance Sheet alongside the Financial Balance Sheet, and Independent Data Auditors provide assurance on the value, quality, integrity and compliance status of an organization’s data assets.

If the twentieth century was governed by the Financial Balance Sheet, the twenty-first century may increasingly be governed by the Data Balance Sheet.

Naavi

")